Tax saving strategies 2026 go far beyond higher 401(k) limits. For…

2026 401(k) Changes: What High Earners Need to Know

The 2026 401k changes for high earners could significantly impact how professionals in their 50s and early 60s save and manage taxes. New catch up rules, Roth requirements, and higher contribution thresholds mean it is more important than ever to understand how your retirement strategy fits into a broader financial plan. Understanding these updates now can help you avoid missed opportunities and unintended tax consequences later.

Base Contribution Limits Under the 2026 401k Changes for High Earners

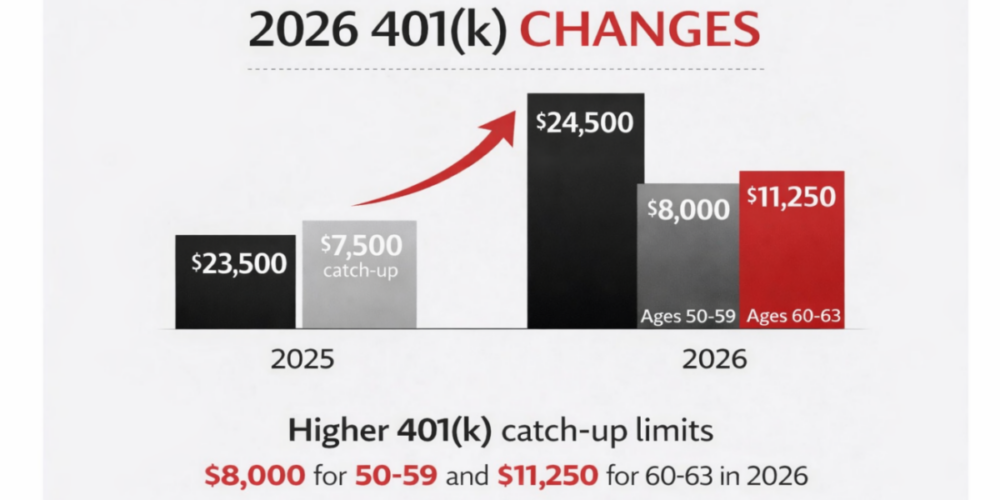

The projected maximum employee contribution for individuals under age 50 is expected to be $24,500.

Two Catch-Up Rules Now Exist

- Ages 50–59 & 64+: Standard catch-up of approximately $8,000 above the base limit

- Ages 60–63 (NEW): A higher “super catch-up” of $11,250 designed to accelerate late-career saving

Why the 2026 401k Changes for High Earners Are Reshaping Catch Up Contributions

If your prior-year W-2 income exceeds approximately $145,000 (indexed) you now have to put the catch up in a Roth instead of it counting toward your tax reduction. This limits your ability to reduce your taxable income.

- Catch-up contributions must go into Roth

- You lose the current tax deduction

- You gain tax-free income later

This shift makes tax planning across account types more important than ever.

The After-Tax Layer Many are Unaware of

Some employer plans allow after-tax (non-Roth) contributions in addition to:

- Base deferrals

- Catch-up contributions

- Employer match or profit sharing

When available, this can help participants approach the full annual limit and supports advanced strategies such as the Mega Backdoor Roth. Availability is entirely plan-specific and often misunderstood.

The $72,000+ Number You May Be Hearing

The total 401(k) contribution ceiling (employee + employer + after-tax, where available) is projected to rise toward approximately $72,000+.

It is important to note that individuals do not personally contribute this entire amount. The total is reached through a combination of:

- Your employee deferrals

- Catch-up contributions

- Employer contributions

- After-tax contributions (if allowed by your plan)

Should everyone max out this amount?

Not necessarily. Unstructured maximum funding can create several challenges, including:

- Liquidity strain

- Over-concentration in pre-tax accounts

- Future tax compression through RMDs

- Reduced flexibility before age 59½

A 401(k) is only one component of a broader, coordinated tax strategy. To see how additional planning layers can enhance long term savings and flexibility, click here for our next article or reach out to schedule a conversation with the CAM Investor Solutions team.

About CAM Investor Solutions

CAM Investor Solutions, a fee-only independent Registered Investment Advisor, has offices located in Colorado, Florida, and Texas. As a growing wealth management firm, we focus on the needs of our clients to improve their quality of life. Our firm’s commitment to innovation through rigorous academic research enhances how we serve a multi-generational audience.

CAM’s Specialties Include:

- Managing concentrated wealth

- Planning for stock and option compensation / company IPOs

- Advanced tax managed investment strategies

- Custom retirement income strategies

- Cash management

Contact:

CAM Investor Solutions

info@caminvestor.com

1-844-247-0787

https://caminvestor.com

CAM Disclosure

SOURCE: Bloomberg; Standard & Poor’s; J.P. Morgan Asset Management.

M & A Consulting Group, LLC, doing business as CAM Investor Solutions is an SEC registered investment adviser. As a fee-only firm, we do not receive commissions nor sell any insurance products. We provide financial planning and investment information that we believe to be useful and accurate. However, there cannot be any guarantees.

This blog has been provided solely for informational purposes and does not represent investment advice. Nor does it provide an opinion regarding fairness of any transaction. It does not constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy.

Past performance is not a guarantee of future results. Diversification does not eliminate the risk of market loss. Tax planning and investment illustrations are provided for educational purposes and should not be considered tax advice or recommendations. Investors should seek additional advice from their financial advisor or tax professional.

Related Posts