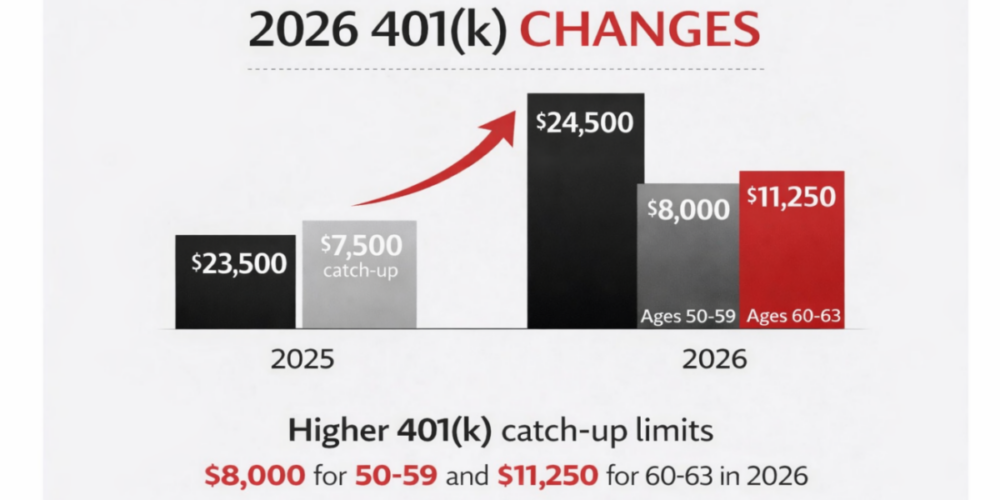

Tax saving strategies 2026 go far beyond higher 401(k) limits. For…

Being Offered a Voluntary Severance Package: Should You Take It?

As you approach the later stages of your career, the prospect of early retirement might suddenly become a tangible option—especially if you’re presented with a voluntary severance package. Such offers can be appealing, promising not only a well-deserved break from the grind but also a potential financial boost. However, the decision to accept a separation package requires careful thought and planning, especially if you have a significant nest egg and are accustomed to a certain lifestyle. Here’s a comprehensive guide to help you navigate this decision.

Evaluate Your Financial Health

Understand the Voluntary Severance Package’s Details

Look closely at what the package offers. Does it provide a severance pay that reflects your years of service and position? How will it affect your pension and ongoing health benefits? Sometimes, the devil is in the details, such as the tax implications of a lump-sum payment which could see you facing an unexpected tax burden.

Financial Impact

Start by assessing your expected monthly expenses in retirement. Can the income from your retirement package, combined with your savings and investments, comfortably cover these costs? Remember, your lifestyle choices will directly impact these calculations. This is a good time to look to a financial plan to see how this outcome will affect your financial longevity.

Review Your Savings

- Ensure that your emergency fund is robust and that your investments can sustain a longer retirement than you might have initially planned. This is crucial if you have a significant amount in investable assets.

- Assess whether your savings, including 401(k), IRAs, and other investments, are adequate to fund your retirement, potentially earlier and longer than initially planned.

- Access to Retirement Funds: If you’re retiring before age 59½, consider how you will access retirement funds without incurring penalties, or if it’s necessary to adjust your withdrawal strategy. A long term cash flow strategy as part of your financial plan can help you with this.

Tax Implications

Generally, severance pay is treated as ordinary income and is taxed at your usual income tax rate. This means that the lump sum you receive could potentially push you into a higher tax bracket for the year you receive it, resulting in a higher tax liability. Taxes are typically withheld from your severance pay at the standard rate. However, because severances can sometimes be paid in a large lump sum, the withholding may not cover the total tax bill. You might need to make estimated tax payments to avoid underpayment penalties. Also, high-income earners may be subject to an additional Medicare surtax. The additional income from a severance package could potentially push you over the threshold for this surtax. If you are concerned about this, be sure to consult your accountant or advisor for additional help.

Health Insurance and Benefits

Healthcare is a critical factor, especially as you age. If your voluntary severance package doesn’t extend health benefits until you are eligible for Medicare, you may need to look into alternative options such as COBRA or private health insurance. Also, consider the impact on other benefits you may be losing, like life and disability insurance.

Personal Considerations

When considering an early retirement, it’s crucial to assess both your age and health, as well as your lifestyle goals. Are you physically and emotionally prepared to retire? If you accept the voluntary severance, would you retire or find another job? If you choose to retire now, remember that you may need to wait to access key benefits such as Social Security and Medicare. What if you choose to keep working after your severance? Be sure to check if there are any non-compete clauses or restrictions on working in the same industry post-retirement, which could limit your future job opportunities. Making these considerations will help you determine if early retirement truly aligns with your personal and financial objectives.

Taking an early retirement package can be a pivotal decision in your financial and personal life. It’s not just about ending a career; it’s about beginning a new chapter with confidence and stability. At CAM Investor Solutions, we’re here to help you analyze your options and make the best decision based on your unique financial situation and retirement goals. Contact us today to discuss how we can assist you in making this transition as smooth and beneficial as possible.

Disclosure

M & A Consulting Group, LLC, doing business as CAM Investor Solutions is an SEC registered investment adviser. As a fee-only firm, we do not receive commissions nor sell any insurance products. We provide financial planning and investment information that we believe to be useful and accurate. However, there cannot be any guarantees.

This blog has been provided solely for informational purposes and does not represent investment advice. Nor does it provide an opinion regarding fairness of any transaction. It does not constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy.

Past performance is not a guarantee of future results. Diversification does not eliminate the risk of market loss. Tax planning and investment illustrations are provided for educational purposes and should not be considered tax advice or recommendations. Investors should seek additional advice from their financial advisor or tax professional.

Related Posts