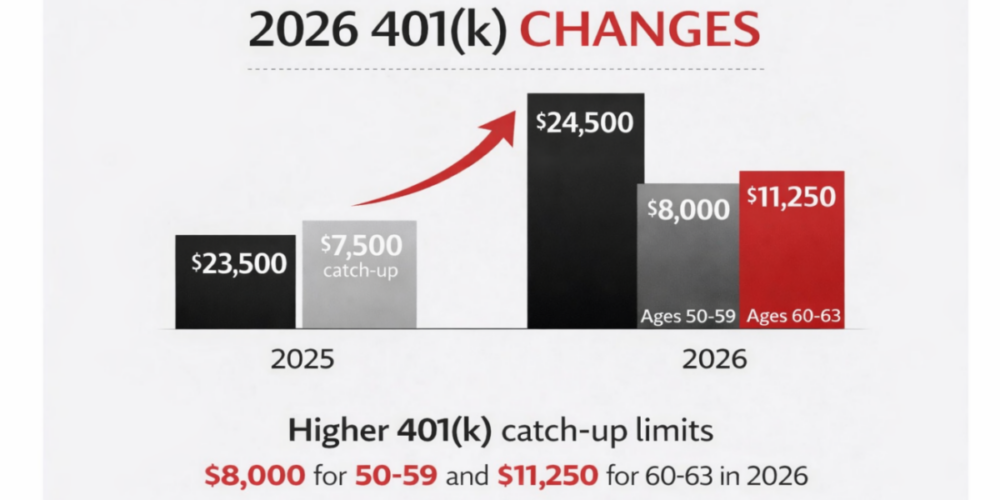

Tax saving strategies 2026 go far beyond higher 401(k) limits. For…

Changing Jobs – What to do with your old 401(k)?

If you live in the South, like we do, this summer’s heat may have you considering a relocation and job change just to find cooler weather. In all seriousness though, if it’s something you’ve been thinking about for a while (leaving your current job) and the new opportunity is right, go for it! Let the excitement of a new adventure outweigh the fears or concerns you may have related to the many other changes coming your way. When you leave your old employer all your benefits will change, which can be daunting. Your health insurance coverage will be different, as will your life and disability insurance. And what about time off? Maybe least of your immediate concerns is the retirement account you’ll be leaving behind. If you need, take your time but don’t forget about this valuable savings you’ve set aside for yourself. So what do you do with your 401(k) or retirement plan from your old employer?

3 Options

There are three options (and sort of a 4th, but it’s not recommended) you can choose from when you leave your old employer, and each one has it’s pros and cons. Depending on your circumstances will determine which is the right option for you. Still don’t know which is the right option for you after reading this blog? Reach out to a financial advisor and they can help guide you.

- Option 1: Leave your plan with your former employer – Many plan sponsors allow you to keep your retirement savings in their plans after you leave.

- Option 2: Convert the money into an IRA. – You can open an IRA with a bank or brokerage firm and move, or roll over, the money into it. Make sure to research fees and expenses when choosing an IRA provider, though. They can really vary.

- Option 3: Transfer your plan into a new employer’s plan. – Employers often will accept a rollover from a previous employer’s plan, so check with your new employer before making any decisions.

- Option 4 (NOT advised): Take your money out of your retirement account completely. This can be a costly option since withdrawals of cash are subject to taxes and penalties. Leaving your money in a tax-advantaged retirement account preserves the tax benefits and can help your savings grow over time.

Which Option is Right for You?

Leave It

If your new employer does not offer a retirement plan or does not allow you to roll over your old 401(k), then you may want to leave it with your old employer. Another reason to leave your money where it is could be low fees. Many retirement plans offer institutional class shares, which generally have lower fees. They also offer a decent line up of fund options to choose from.

Need your money a little early? No problem if you’re 55 and you want to pull money out of an employer sponsored retirement plan; it’s penalty free at age 55. For an IRA you must be 59 1/2 to withdraw funds to avoid a penalty. The assets in your 401(k) are also better protected from lawsuits under federal law, where IRAs are not.

The cons to leaving your retirement funds with your old employer are mainly the hassle of having multiple accounts in different locations, and possibly NOT great investment options. If you move your money to an IRA, your investment options are nearly limitless – which is not the case with employer provided retirement plans.

Convert It

Moving your money to an IRA will give you the most flexibility and control of your investments and fees. Whether you manage the IRA yourself, or you have a financial advisor manage your money – you will be able to invest in stocks, bonds and private assets. With more investment options, you may be able to better diversify your portfolio and choose investments that will help you achieve your goals. Additionally, having your assets all in one place may make it easier for you to manage your investments asset allocation.

One thing most people don’t consider when making this decision is tax planning and long-term investment limits. If you are a high-income earner, or expect to be in the future, you will eventually be ineligible to contribute to a Roth IRA. However, if you have a $0 balance in any/all your IRA accounts or you don’t even have one, you can still make Roth IRA contributions through what’s called a “backdoor” Roth conversion.

In order to complete this conversion without incurring a tax bill for the conversion, you must first contribute no more than the amount allowed for that year to an empty IRA. Once the money has settled in the IRA, then you want to perform a Roth conversion for the entire amount in the IRA you just deposited, into your Roth IRA account. If you roll your 401(k) account into an IRA, you will not be able to perform a backdoor Roth conversion.

Transfer It

Having all your retirement funds in one account can help increase your growth better than if they were separate, due to compounding. Want to know more about how compounding works? We wrote a blog about it here. Many retirement plans allow current employees to take a “loan” from their own 401(k) account at lower rates than you may find at a bank. The amount you can borrow is based on the total value of your account and is limited to 50% of the value, with a max loan of $50,000. If you roll over an old retirement plan, you’ll be able to reach that max amount ($100,000 balance to get a loan for $50,000) sooner.

If you want to roll your old retirement account to your new employers plan, make sure it’s a “direct rollover”. This will avoid any taxes or penalties. A check will need to be sent directly to your new plan addressed as “For the Benefit of [YOUR NAME]”. If you have any concerns or questions, reach out to your new Benefits team or your former 401(k) plan team.

Turn in Your Notice

A new adventure awaits! Don’t let the concern for your old retirement account stop you. Turn in that notice and take a few weeks to think over your decision. This is not the time to make a haste decision – once you roll out of your old employers 401(k), you cannot go back (unless you work there again later). Still have questions about whats best for you and your specific situation? Reach out to a trusted fee-only financial advisor for guidance.

Disclosure

M & A Consulting Group, LLC, doing business as CAM Investor Solutions is an SEC registered investment adviser. As a fee-only firm, we do not receive commissions nor sell any insurance products. We provide financial planning and investment information that we believe to be useful and accurate. However, there cannot be any guarantees.

This blog has been provided solely for informational purposes and does not represent investment advice. Nor does it provide an opinion regarding fairness of any transaction. It does not constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy.

Past performance is not a guarantee of future results. Diversification does not eliminate the risk of market loss. Tax planning and investment illustrations are provided for educational purposes and should not be considered tax advice or recommendations. Investors should seek additional advice from their financial advisor or tax professional.

Related Posts