Tax advantaged investment strategies are becoming a priority for high-net-worth investors…

Personal Finance Basics for your Grad

When someone asks “what do you do for a living?” and I answer “I’m a financial advisor” most people either respond with an “eh” or “I wish they offered a personal finance class when I was in high school.” It still astonishes me that so many people respond with this second comment. Not because I didn’t know these types of courses aren’t offered or required to younger folks, but because people WISH they were! And good for them. It’s never too late to learn the basics of personal finance.

Do you have a grown child that’s just finished college or is moving out on their own for the first time? If so, this would be a great time to impart a few basic financial pearls of wisdom to help them be financially independent and successful. You can use this as a guide to share your own experiences. Tell stories of how you have achieved financial success or are close to financial freedom.

The Basics

Income & Expenses

When you read a book, what page do you start on? Have you ever jumped right to the middle and read through to the end, trying to figure out what the first half was about? I’m guessing you haven’t. The same goes with your personal financial situation. You need to start at the beginning – which is, where does your money come from? How much money do you earn? How often are you paid? What is deducted from your paycheck? If you don’t know the answers to these questions, it will be very hard for you to know how much you can SAVE, SPEND, and GIVE/WANTS. These are the three basic principals to budgeting.

SAVE – this is where most people need the biggest help. Not saving enough can quickly lead to all kinds of debt. So this is where you should start. The 50/30/20 Rule says you should save 20% of each paycheck. This 20% of savings is for your emergency money and future goals, like buying a house, retirement or a special event.

SPEND – next you’ll need to spend money on your needs. The 50/30/20 Rule says about 50% of your income should go to basic necessities like housing, food (at home – not restaurants), child care, taxes, insurances, etc. Think of the bills you must pay or someone will come knocking on your door – those fall into this category.

GIVE/WANTS – the last bit of your money, the remaining 30% can be spent on things you want or giving to others. If your interested in philanthropy, you might use more of this last bucket to donate to a cause you feel passionate about. At the same time, it’s also completely acceptable to spend this 30% on something you want, like a vacation you’ve wanted for years. Or the latest book by your favorite author.

The key to being successful with the 50/30/20 Rule is to know your numbers. Try to stay within these bands. If you do, you’ll be on your path to financial success and achieving your goals.

Saving

Life is unpredictable. You never know when you might need some extra cash if you lose your job, get sick or have to take care of a family member. The extra cash you should have saved up for these events is called your “emergency fund”. It’s recommended that you have 3 – 6 months of your expenses saved in this account. For example, if you spend $5,000 a month you need to have $15,000 – $30,000 in a savings account. This is money you don’t touch. It’s for an emergency! But that doesn’t mean your money can’t be working for you. Now that rates have risen, you can earn some interest on this account. Shop around for a high yield savings account. These accounts will pay you an APY – as explained in the Investopedia article above.

Beyond this emergency fund, you should also save through investment vehicles like an employer retirement plan. This might be a 401(k), 403(b) or pension. If your employer provides a match (i.e. you put some in, and they’ll put in the same amount), you should definitely do it. This is free money! Even if you can’t “max out” your contributions, put in enough to get the match. The younger you start, the less you have to save each month compared to starting later in life. This is the beauty of compounding, which you can read more about in one of our previous blogs.

Borrowing

Every now and then we need or want to buy something we don’t have enough money for. This might be new clothes, a special gift or a fancy meal out. Many people get introduced to credit cards for the first time when they go to college. But they don’t know anything about how they work. They think – free money! While they can be useful and we sort of need them to build credit, they can also be a very slippery dangerous slope. New credit card users need to understand what interest is. What is the rate? How is it calculated? When do you have to pay it?

Investopedia has a great article that explains APR vs APY. In this article they teach you how to calculate APR, the interest rate that credit cards charge. Before you are enticed by credit card perks and apply, make sure you know and understand what the APR is.

If you can purchase things with a 0% interest rate, that’s great! But make sure you read the fine print. Usually this 0% rate is only for a certain amount of time, and if you slip up and miss one payment, you have to pay ALL the interest over the entire life of the loan at a higher rate.

Investing

As wealth advisors we are often asked how one should learn about investing. Is there a book they should read? Should they pick individual stocks? Is it ‘safe’? Is now the right time? We provide guidance tailored to the inquirers personal circumstances, as these answers are generally different for each individual.

There is one book, however, that we recommend to everyone. The Psychology of Money by Morgan Housel. This book is a short, easy read that lays out basic investment principals. Through stories Housel is able to help the reader truly understand financial content that would otherwise be found in a college textbook.

And is now a good time? Yes! The sooner the better. Not to be repetitive, but if you read our blog about compounding, you’ll see how important time is. And by waiting a year or two, you will potentially be missing out on a larger future portfolio value just due to time. You don’t need to have a lot of money to invest, just start with what you can spare in your budget.

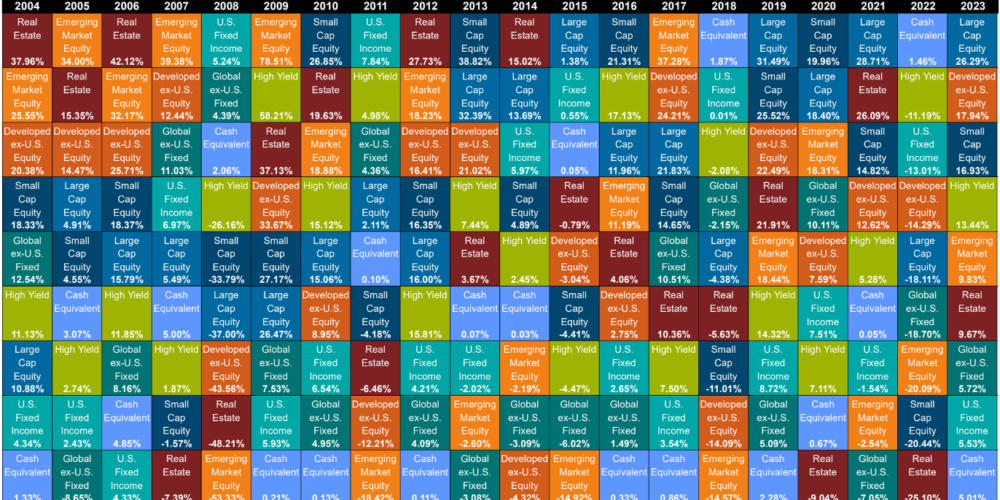

What should you invest in? Again, that depends on each persons financial situation, goals and risk tolerance. If you can, you should work with a CERTIFIED FINANCIAL PLANNER™ professional to help guide your investment decisions. If you’re not able to, then you should at least stick with broadly diversified passive investments. Investments like index funds are a good start.

Share the Knowledge

Congrats to you for having raised a child that has launched. They’re leaving the nest to be independent. Give them one more parting gift – knowledge. Pass along these personal finance basics so that they may help themselves. Teach them how to fish.

Disclosure

M & A Consulting Group, LLC, doing business as CAM Investor Solutions is an SEC registered investment adviser. As a fee-only firm, we do not receive commissions nor sell any insurance products. We provide financial planning and investment information that we believe to be useful and accurate. However, there cannot be any guarantees.

This blog has been provided solely for informational purposes and does not represent investment advice. Nor does it provide an opinion regarding fairness of any transaction. It does not constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy.

Past performance is not a guarantee of future results. Diversification does not eliminate the risk of market loss. Tax planning and investment illustrations are provided for educational purposes and should not be considered tax advice or recommendations. Investors should seek additional advice from their financial advisor or tax professional.

Related Posts