"Do not mistake a confident explanation for an accurate prediction" - James Clear. It's important to remember this when reading the news.

Q4 2022 – The Capital Markets Don’t Care About Talk

Like any good comeback story, the market had a strong finish in the Fourth Quarter. Unfortunately it was not enough to put stocks and bonds in the green for 2022.

Whether the lows reached in October prove to be the turning point in the recent downturn remains to be seen, but it’s certainly encouraging that the inflation rate has been steadily declining since it reached a 40-year high last June. If that trend continues, it will take much of the pressure off the Federal Reserve to keep hiking interest rates, which will likely boost stocks and will most certainly boost bonds.

As we’ve seen recently, bonds aren’t immune to volatility, they’re just historically less volatile than stocks. Likewise, cash investments are less volatile than bonds. The trade-off for lower volatility is, of course, lower expected returns than riskier assets like stocks historically have delivered. Bonds will never eliminate volatility in a portfolio, but historically they’ve proved to be a much better asset class than cash to balance risk and return when seeking to reduce stock volatility.

Whenever stocks and bonds decline together, as they did in 2022 as well as 2020, the chatter predictably starts that “the 60/40 portfolio is dead.” This is another way of saying that diversifying into fixed income to reduce portfolio volatility doesn’t work anymore, even though it’s always worked in the past.

This is not a new, hot take. We hear this claim every time stocks and bonds decline simultaneously, and every time the idea that diversification into fixed income doesn’t work anymore has proven to be completely false. We have no reason to believe otherwise this time.

It’s also very important to note that not all fixed income is created equal. The bond market is much bigger than the global equity markets. This consists of both traditional bonds and nontraditional bond strategies, which had significantly different performances in 2022. To some investors’ surprise, many fixed income strategies did just fine as interest rates were on the rise last year. You had to know just where to look and how to properly diversify your portfolio in line with your long-term financial planning goals and objectives.

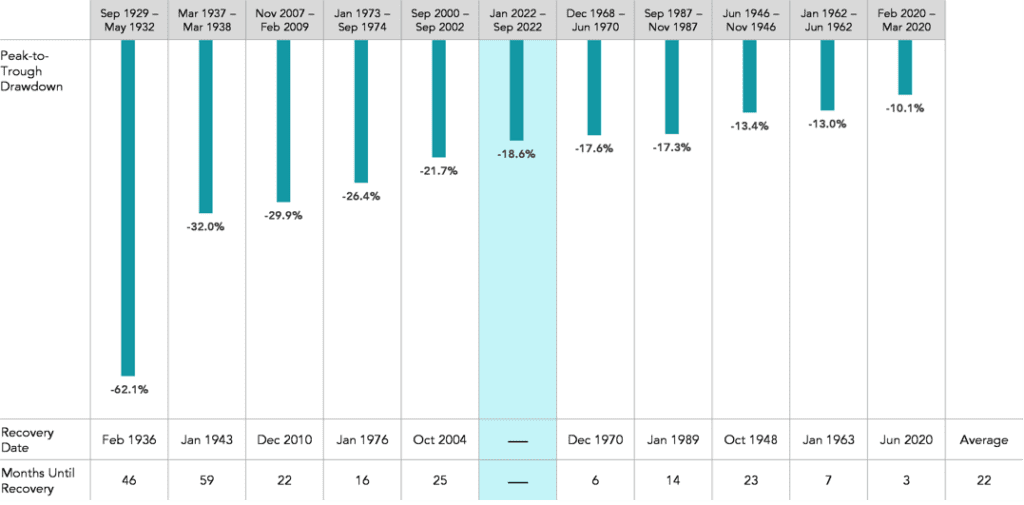

The graph below shows the most significant peak-to-trough declines for a hypothetical portfolio invested 60% in the S&P 500 index and 40% in five-year Treasury notes since 1926. As you can see, the current decline (shaded in blue) is roughly in the middle of the pack and not out-of-the-ordinary when compared to similar bear markets of the past:

Historical 60/40 Returns (January 1926 – September 2022) 1

While the average recovery time for those downturns is 22 months, that average is heavily skewed by the extreme Depression-era bear markets. Most recoveries were significantly shorter than the average.

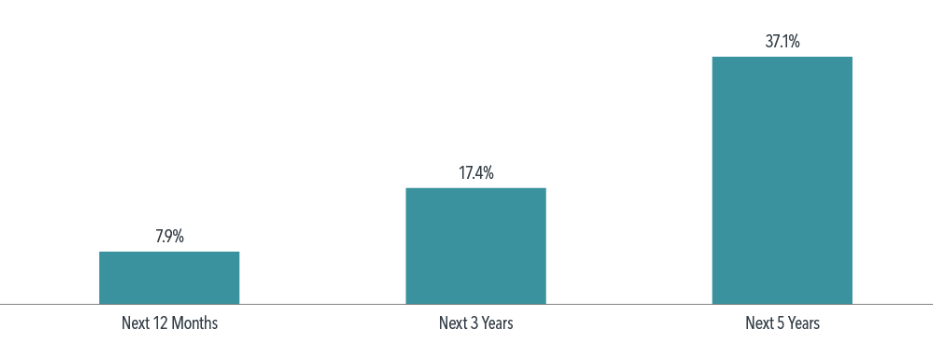

Moreover, once those downturns run their course, they are historically followed by robust recoveries:

Historical Returns for 60/40 portfolio

after 10% declines (January 1926 – September 2022) 2

The assertion that fixed-income diversification is “dead” doesn’t reflect some new reality. It only reflects a fundamental lack of understanding about the benefits – and limits – of using bonds to reduce portfolio risk.

If you embrace the idea that bonds somehow no longer work to reduce volatility, the question then becomes: What does? In recent years, many of these investors have turned to cryptocurrencies as an alternative to the fixed-income positions in their portfolios.

Yes, you read that right. There has been a growing chorus of pundits in recent years making the claim that crypto is a better hedge against stock volatility than bonds. Advocates of this strategy claimed that crypto had both a much higher upside than bonds and was also much safer than bonds.

One article by Bitcoin advocate Mimesis Capital on the Nasdaq website on April 16, 2021 included this assertion:

“Bitcoin can be viewed as the most antifragile asset in the modern financial system, whereas bonds may be viewed as the most fragile asset in the financial system.”

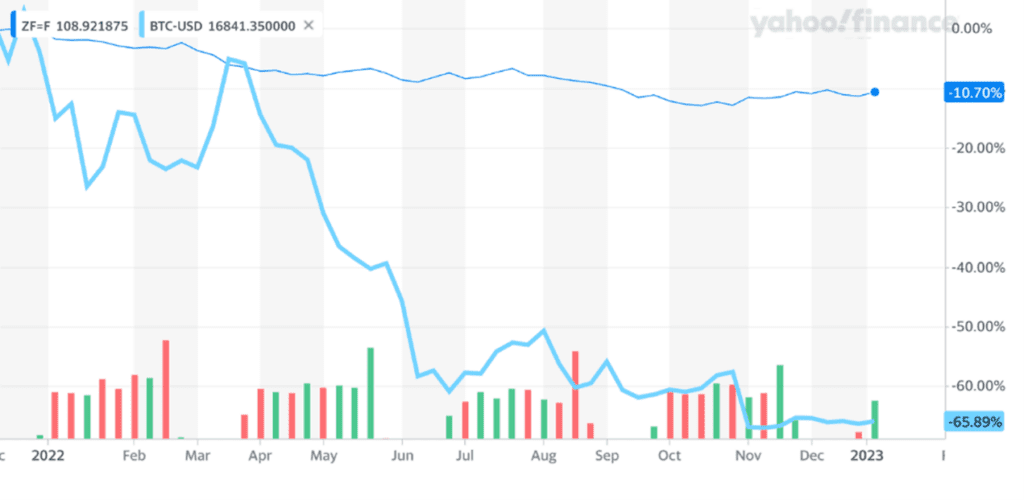

So…let’s check the tape and see how that worked out, shall we? Below is a chart comparing the one-year return of the five-year Treasury note (symbol ZF=F) and Bitcoin (symbol BTC) through 12/31/22:

If Bitcoin is the modern financial system’s “most anti-fragile asset,” it apparently did not get the memo, plunging more than 65% in 2022. And Bitcoin actually fared better than many of its crypto counterparts, which lost somewhere between 70% and everything in the meltdown that ensued after the alleged fraud perpetrated by crypto exchange firm FTX Trading came to light in November.

As they say, talk is cheap, and in no arena is it cheaper than investing. People can, and do, make all manner of outrageous claims about being in a “new era” where the time-tested ways of managing money are dead and the new way is the only way. We heard it in the late 1990s during the dot-com bubble, in the real estate bubble in the mid-2000s, and now with the crypto craze in recent years.

The capital markets don’t care about talk – they deal only in reality. And the reality is that the crypto market is largely illiquid, opaque and under-regulated. Those who convinced themselves that crypto was a safe alternative to bonds got a heavy dose of that reality in 2022.

Is your portfolio ready for what 2023 has in store – whether that’s a continuation of the Q4 comeback or more the same as 2022? We are happy to take a look and give you a 2nd opinion if you’re not sure. It’s easy to set up a call with us through our online calendar. Let us help you be ready!

1 Past performance is no guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. The 60/40 Portfolio is comprised of the S&P 500 Index (60%) and Five-Year US Treasury Notes (40%). Rebalanced monthly. The maximum drawdown shows the largest decline in the value of the investment or index since the first full month of the investment or, in the case of an index, since the first full month of the oldest investment in the comparison. Peak is the highest point prior to the drawdown, trough is the lowest point after the peak, and recovery is the date, if any, that the investment or index reached or surpassed the peak. Five-Year US Treasury Notes data provided by Morningstar. S&P data © 2022 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Source: Dimensional, Inc. and Morningstar Direct as of September 30, 2022

2 Past performance, including hypothetical performance, is not a guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. In USD. The 60/40 Portfolio is comprised of the S&P 500 Index (60%) and Five-Year US Treasury Notes (40%). Rebalanced monthly. 60/40 Portfolio declines are defined as periods in which the cumulative return from the prior peak is –10% or lower for the 60/40 Portfolio. Returns are calculated for the 1-, 3-, and 5-year look-ahead periods beginning the month after the respective downturn thresholds are exceeded. The bar chart shows the average cumulative returns for the 1-, 3-, and 5-year periods post decline. There are 10, 9, and 9 observations for the 1-, 3-, and 5-year look-ahead periods, respectively. Five-Year US Treasury Notes data provided by Morningstar. S&P data © 2022 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Source: Morningstar Direct as of September 30, 2022

M & A Consulting Group, LLC, doing business as CAM Investor Solutions is an SEC registered investment adviser. As a fee-only firm, we do not receive commissions nor sell any insurance products. We provide financial planning and investment information that we believe to be useful and accurate. However, there cannot be any guarantees.

This blog has been provided solely for informational purposes and does not represent investment advice or provide an opinion regarding fairness of any transaction. It does not constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Past performance is not a guarantee of future results. Diversification does not eliminate the risk of market loss. Tax planning and investment illustrations are provided for educational purposes and should not be considered tax advice or recommendations. Investors should seek additional advice from their financial advisor or tax professional.

Related Posts