How proactive tax planning can improve long term investment goals. Wondering…

Ready, Set, File: Don’t let tax season catch you off guard

“You must pay taxes. But there’s no law that says you gotta leave a tip.” ~ Morgan Stanley. Would you like to pay less in taxes or at least not pay more than you have to? I think we all raise our hand for that! How do you achieve this? By being proactive! If you just let your taxes be what they will, you may be missing opportunities to save more and pay less in taxes. You don’t need to leave a tip!

Most of our tax planning techniques are not useful for the previous year if they are enacted after December 31st. But there are still a few that we can take advantage of if used before tax filing day – April 15th, for most. As we navigate through the year, staying ahead in our tax planning is crucial for financial health and peace of mind. From January until the tax deadline, several key dates stand out as opportunities to manage, assess, and strategize your tax situation. Here’s a comprehensive guide to help you stay on top of your taxes in 2024.

January: Kickstart Your Tax Planning

Important Dates

Do you feel more invigorated after the holidays – ready to tackle the new year and get back to work? Or maybe, you’re a little more sluggish and not quite ready to “hit the ground running”. Good news for you later bunch, there’s nothing you really HAVE to do in January related to taxes. Employers are getting their documents together, and unless you own a business, you just have to wait for that W-2 to arrive.

- January 1: The start of the new tax year. Review your financial resolutions and set clear, achievable goals.

- January 31: Deadline for employers to send out W-2 forms and for businesses to issue 1099 forms to non-employees.

For you energized new years folks – take this time to start planning what 2024 holds for you!

Tips

- Organize Your Documents: Gather all necessary documentation, including W-2s, 1099s, and receipts for deductions.

- Review Your Financial Transactions: Look for any transactions that could impact your tax situation, such as selling property or withdrawing from retirement accounts.

February: Fine-Tune Your Strategy

There are no specific IRS deadlines, but February is also a good time for review. Maybe you didn’t get started in January, that’s okay. But now you really should start thinking about your taxes and planning.

Tips

- Consult a Professional: Consider meeting with a tax advisor to discuss your financial situation and any tax law changes that may affect you. CPAs are becoming harder to find – too many people to help, not enough new CPAs each year. I’d find a CPA sooner than later.

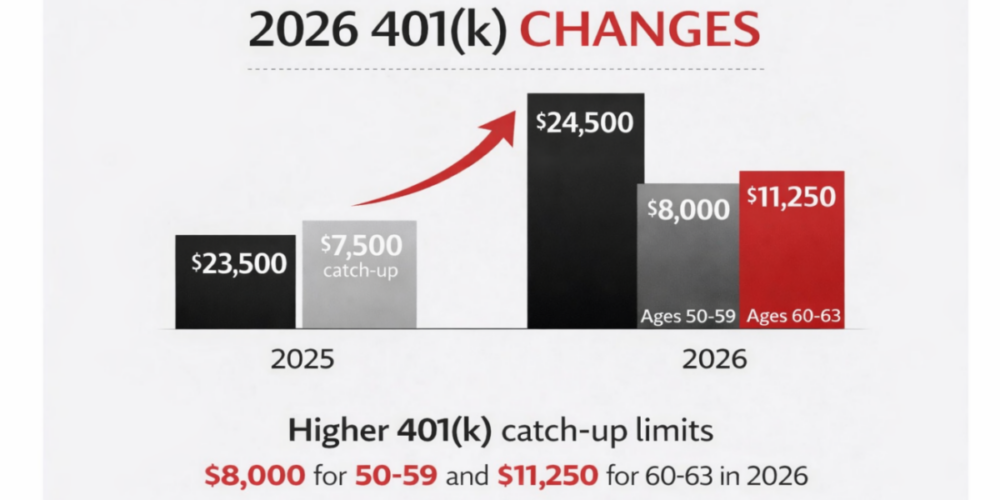

- Contribute to Retirement Accounts: Maximize contributions to your IRA (Traditional, Simple, SEP) to reduce your taxable income. You can also still make contributions for your Roth IRA before April 15th.

March: Last Call for Deductions and Contributions

Most of the forms you need to file should have arrived by now. If you’re ready, go ahead and file so you check taxes off your to-do list. If you’re expecting a return, it’s better to file sooner to reduce the time it will take to get your refund.

Important Dates

- March 15: Deadline for corporate tax returns (Forms 1120, 1120-A, and 1120-S)

Tips

- Maximize Deductions: Ensure you’ve taken advantage of all eligible deductions, including charitable donations and business expenses. This may be tedious work, but you will literally “pay” yourself for the time if you’re able to itemize and reduce your tax bill.

- Health Savings Account (HSA) Contributions: If you have an HSA, ensure you’ve contributed the maximum amount. HSAs are becoming extremely helpful retirement accounts, since you don’t lose your contributions annually, and the money can be invested and grow tax free. Even better, contributions can reduce your current taxes and can be made all the way up until April 15th for the previous year, if you were in a high deductible health plan for the previous year!

April: Final Preparations and Filing

No more procrastinating, the big tax month is finally here! At this point if you don’t have a CPA, you’ll likely need to do your own taxes or use an automated system like TurboTax or find an authorized e-file provider directly on the IRS’s website.

Important Dates

- April 15: Tax Day! Individual tax returns due, or request an extension. Also, the deadline for first-quarter estimated tax payments.

Tips

- Double-Check Your Return: Ensure all information is accurate to avoid delays or audits. We can’t stress this enough – taxes are complicated and you don’t want to miss out on any credits, or underreport your earnings. If you don’t feel confident with the numbers you’ve got, please utilize tax software or a professional to help.

- Plan for Next Year: Doing taxes not your thing? Want to do it better next year? Set up a system for organizing your 2024 financial documents to make next year’s tax season smoother. Set a meeting with both your financial advisor and accountant to review strategy for the upcoming year.

By marking these important dates on your calendar and following these tips, you can navigate the tax season with confidence and efficiency

Tax planning techniques to consider for next year

If you don’t want to leave the government a tax tip, what can you do to lower your 2024 tax bill? Starting early and having a plan is the first step. At CAM we believe that tax planning is necessary and a key part of all our clients financial plans. Every action should include the question – how does this affect my taxes, in the near-term and also much further into the future?

These are a few of the tax planning tools we consider and employ for clients:

- Monthly investment contributions: By adding money each month to your brokerage account, you’ll be able to invest at different market prices. These different market prices will allow for tax-loss harvesting opportunities when the eventual market downturn occurs. By starting this process early, you can save up years of tax-losses. How is this helpful? If you have a big gain in one year from the issuance of company stock or a real estate sale, these saved losses can make that year not so painful on your tax return

- Tax-loss harvesting: We don’t sit and watch portfolios daily, but we do use tools that help us monitor market prices. If they swing too much in one direction, we evaluate if a portfolio could capture a tax benefit due to the market prices moving.

- Charitable giving: The IRS has made the standard deduction amount so high, it’s not always possible to itemize taxes to get a bigger break. What if you stacked up two years worth of charitable giving into one year? Maybe this year you put that charitable gift amount into a high-yield savings account to grow. Then give it to your charity of choice in 2025 along with what you planned to give in 2025? This year you take the standard deduction you would have taken anyway, but for 2025 you can itemize!

- Charitable giving over age 70 1/2: Most of us don’t want to get older, but sometimes their are perks. Anyone over the age of 70 1/2 can make charitable gifts directly from your IRA or 401(k) to a charity. When given directly, it does NOT count as income and you still get the tax benefit of giving to a charity!

- Retirement contributions: Did you know that you can lower your taxes by contributing to your employers retirement plan? If you choose to make pre-tax contributions, you could possibly even lower what tax bracket you’re in. You’ll want to start contributing earlier in the year, so you don’t have to use an entire paycheck or two at the end of the year to reduce your annual earnings.

- Quarterly payments: If you are self-employed, you can avoid over-paying the government by avoiding fees. By withholding about 30% of each paycheck and paying the IRS quarterly, you can avoid the IRS penalty for not paying enough tax throughout the year.

- Small business retirement plans: Business owners are able to save more for their own retirement, as well as offer a nice employee perk by offering a retirement plan. These plans also have the benefit of lowering personal taxes and business taxes! Open a plan sooner in the year for more savings!

- Real estate sales: Have a rental property you want to get rid of? Have you heard of a 1031 exchange? This is a way to delay paying taxes on the sale, but you’ll want to learn about this BEFORE you sell your property. We can help with these!

And the list goes on! These are just a few of the ways that we help clients plan ahead for how activities and events might affect their taxes. Many things have a tax impact – marriage, kids, buying a new car, updates to your house, company stock! We are here to help our clients with all of these life events.

Remember, proactive planning and early action can make a significant difference in your tax situation, potentially saving you time, stress, and money. Consult your tax, legal, and accounting professionals before modifying your tax strategy, and let us know if you’d like to set aside some time to chat.

Disclosure

M & A Consulting Group, LLC, doing business as CAM Investor Solutions is an SEC registered investment adviser. As a fee-only firm, we do not receive commissions nor sell any insurance products. We provide financial planning and investment information that we believe to be useful and accurate. However, there cannot be any guarantees.

This blog has been provided solely for informational purposes and does not represent investment advice. Nor does it provide an opinion regarding fairness of any transaction. It does not constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy.

Past performance is not a guarantee of future results. Diversification does not eliminate the risk of market loss. Tax planning and investment illustrations are provided for educational purposes and should not be considered tax advice or recommendations. Investors should seek additional advice from their financial advisor or tax professional.

Related Posts