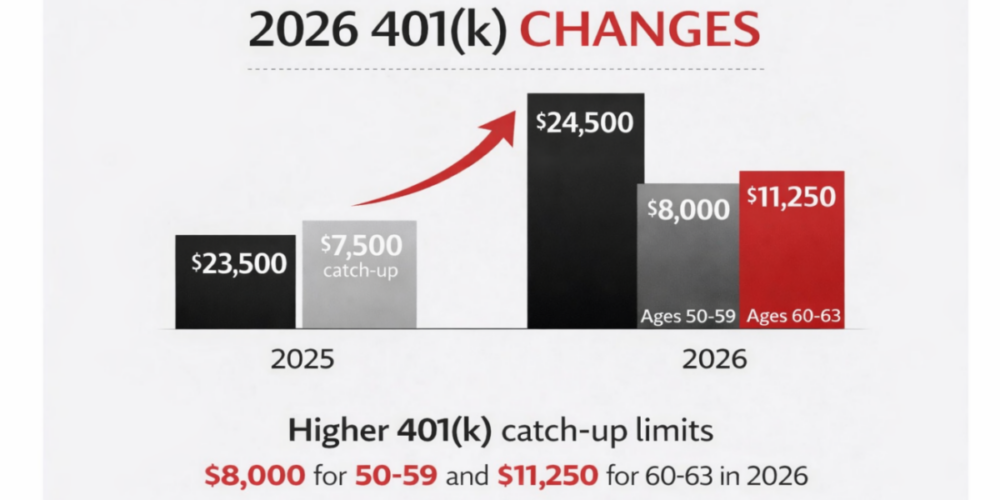

Tax saving strategies 2026 go far beyond higher 401(k) limits. For…

Tax Planning Strategies We Implemented for Clients Last Year

How proactive tax planning can improve long term investment goals.

Wondering how to lower your tax bill? The most effective tax planning strategies happen before year end. Coordinating investment decisions, income timing, and portfolio strategy can meaningfully improve after-tax outcomes over time.

Every year around this time we hear from new clients asking the same question:

What can I do to lower my tax bill?

The most meaningful opportunities rarely happen when you are filing your tax return. They happen months earlier, when a few well timed decisions and thoughtful analysis can improve the long term tax efficiency of your wealth.

Many of these strategies are particularly relevant for investors with significant taxable assets, equity compensation, or multiple income sources.

Below are several tax planning strategies we implemented for clients during the past tax year.

In This Article

- Tax-loss harvesting strategies to reduce capital gains

- Strategic Roth conversions

- Stock options and equity compensation planning

- Diversifying concentrated stock positions

- Tax aware portfolio construction to reduce ordinary income

- Required minimum distribution planning

- Asset location optimization

Tax Planning Strategies Often Used by High Income Investors

High income investors often face complex tax situations that require proactive planning throughout the year. Common tax planning strategies include reducing capital gains exposure, implementing Roth conversions during lower income years, coordinating equity compensation events, optimizing asset location across accounts, and structuring portfolios to improve after tax efficiency.

When these strategies are coordinated with a long term investment plan, investors can reduce lifetime tax exposure while maintaining diversified portfolios aligned with their financial goals.

1. Capital Gains Management (Not Just Loss Harvesting)

The Situation

Markets create both gains and losses across portfolios. In certain years, appreciated positions and rebalancing needs can generate meaningful capital gains exposure.

The Strategy

We harvest losses where appropriate, but we also sometimes strategically realize gains during lower income years to intentionally reset cost basis.

During higher gain years, we may apply existing capital loss carryforwards to offset realized gains while still making necessary portfolio adjustments.

The Impact

Lower embedded tax risk

Improved portfolio flexibility

Greater control over the timing of taxable events

Our focus is not just reducing this year’s tax bill but managing the long term tax trajectory of the portfolio.

2. Strategic Roth Conversions

The Situation

Clients sometimes experience temporary lower income years such as:

- Early retirement

- Career transitions

- Business revenue fluctuations

These periods can create opportunities for tax efficient Roth conversions.

The Strategy

We modeled marginal tax brackets and selectively converted portions of pre tax retirement accounts while tax rates were favorable.

The Impact

Reduced future required minimum distributions

Created long term tax diversification

Avoided pushing income unnecessarily into higher tax brackets

We evaluate not only the tax impact today but also how these decisions may reduce lifetime tax exposure.

3. Stock Options and Equity Compensation Planning

The Situation

Several clients had large RSU vestings and option exercises scheduled during high income years.

The Strategy

We projected multi year income scenarios and coordinated closely with their CPA to stage exercises where appropriate. This helped avoid stacking equity income on top of bonuses and other peak earnings.

In some cases we paired equity events with tax aware portfolio strategies such as loss harvesting or gain coordination.

The Impact

More controlled marginal tax exposure

Improved planning for estimated tax payments

Reduced concentration risk

Equity compensation was integrated into the client’s broader financial strategy.

4. Diversifying Concentrated Positions Strategically

The Situation

Clients holding highly appreciated single stock positions often face both concentration risk and significant embedded capital gains.

The Strategy

We evaluated structured diversification approaches including:

Staged selling plans

Charitable gifting of appreciated shares

Portfolio strategies designed to gradually reduce risk

The Impact

Reduced single stock exposure while maintaining control over the timing of taxable gains.

5. Tax Aware Portfolio Construction

The Strategy

High income households with significant taxable assets often face ongoing capital gains exposure based on how portfolios are structured.

The Strategy

In certain cases we implemented tax aware portfolio construction strategies such as long short SMAs, direct indexing and customized loss harvesting at the individual security level.

The Impact

Greater flexibility managing annual tax exposure

Improved after tax portfolio efficiency

Broad market diversification without unnecessary taxable events

Coordinated RMD and Inherited IRA Planning

The Situation

Clients inheriting retirement accounts must now follow the 10 year distribution rule under current tax law.

The Strategy

Rather than waiting until the final years of the distribution window, we built withdrawal schedules aligned with other income sources.

The Impact

Smoothed taxable income across years and reduced the risk of large tax bracket jumps later.

7. Asset Location Optimization

The Situation

Many clients hold assets across taxable accounts, traditional retirement accounts, and Roth accounts.

The Strategy

We adjusted asset location so income producing investments were placed in tax advantaged accounts while tax efficient strategies were implemented in taxable portfolios.

The Impact

Improved after tax returns without changing the portfolio’s overall risk exposure.

Why Proactive Tax Planning Matters

Tax efficiency rarely happens by accident.

The most meaningful opportunities are typically identified well before year end. Looking ahead across multiple years allows for better coordination between investment strategy, tax planning, and major life decisions.

As you review your tax return this year, consider whether last year’s outcomes were intentional or passive.

Thoughtful planning can make a meaningful difference over time.

Thinking About Improving Your Tax Strategy?

If you would like a second set of eyes on how your investment strategy and tax picture interact, the team at CAM Investor Solutions is always happy to have that conversation.

Many of the strategies discussed above work best when investment decisions, tax planning, and long term financial goals are evaluated together.

Frequently Asked Questions About Tax Planning for Investors

When should tax planning begin?

The most effective tax planning strategies occur before year end. Waiting until tax filing season usually limits the available options.

What tax strategies help investors the most?

Common strategies include Roth conversions, capital gains management, tax aware portfolio construction, asset location optimization, and coordinated planning around equity compensation or retirement distributions.

____________________________________________________

About CAM Investor Solutions

CAM Investor Solutions, a fee-only independent Registered Investment Advisor, has offices located in Colorado, Florida, and Texas. As a growing wealth management firm, we focus on the needs of our clients to improve their quality of life. Our firm’s commitment to innovation through rigorous academic research enhances how we serve a multi-generational audience.

CAM’s Specialties Include:

- Managing concentrated wealth

- Planning for stock and option compensation / company IPOs

- Advanced tax managed investment strategies

- Custom retirement income strategies

- Cash management

Contact:

CAM Investor Solutions

info@caminvestor.com

1-844-247-0787

https://caminvestor.com

CAM Disclosure

M & A Consulting Group, LLC, doing business as CAM Investor Solutions is an SEC registered investment adviser. As a fee-only firm, we do not receive commissions nor sell any insurance products. We provide financial planning and investment information that we believe to be useful and accurate. However, there cannot be any guarantees.

This blog has been provided solely for informational purposes and does not represent investment advice. Nor does it provide an opinion regarding fairness of any transaction. It does not constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy.

Past performance is not a guarantee of future results. Diversification does not eliminate the risk of market loss. Tax planning and investment illustrations are provided for educational purposes and should not be considered tax advice or recommendations. Investors should seek additional advice from their financial advisor or tax professional.

Related Posts